Let’s get real for a few moments. Health Reimbursement Accounts all start with the best of intentions. Then, someone gets this crazy idea: “What if the HRA Account only pays expenses incurred when the sun was shining and stars aligned. We could save so much money!” That’s a good time to pump the brakes.

As soon as HRA plan design becomes a game, employees are compelled to find ways to “game the system”. So, even though HRA Accounts start with good intentions, where do they go wrong?

What is an HRA?

Let’s start with the basics — what is an HRA? An HRA Account is an employer-funded account set up to assist employees with out-of-pocket medical expenses. An HRA can be used as a tool to encourage employee engagement in health care purchases or even as a retention tool.

Unfortunately, too often, neither of these things happen and employers see over-utilization and misuse of HRA funds by employees.

What do employees think they know about HRAs?

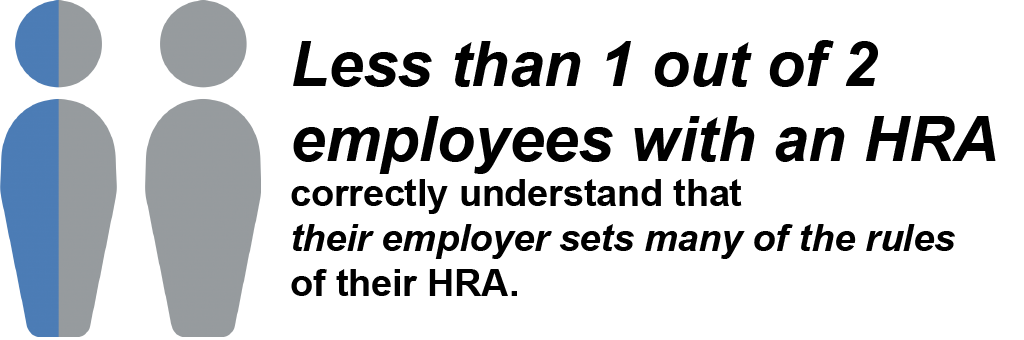

Sadly, many employees with an HRA don’t understand them. Based on the 2018 BRI BRight Ideas quiz, less than one out of two employees with an HRA correctly understand that their employer sets many of the rules of the HRA.

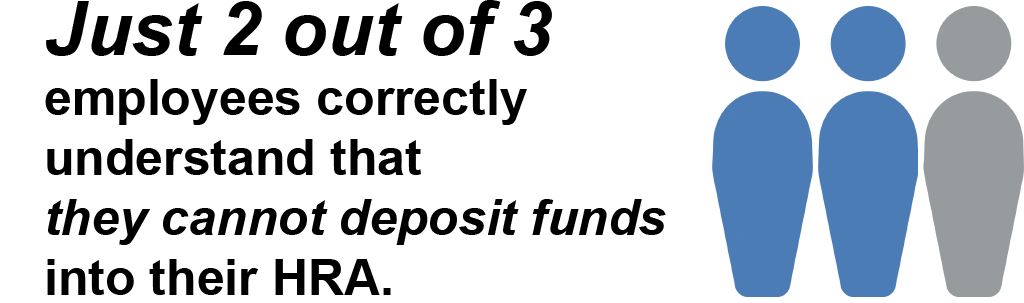

And just two out of three employees correctly understand that they cannot deposit funds in an HRA.

Often, it seems, employees confuse HRAs with HSAs or FSAs. This can lead to some misperceptions.

Misconception 1: Employees often believe an HRA is their money.

Employees may see an HRA Account as a portion of their benefits package and may consider it as part of their overall compensation. This can be a positive interpretation in some ways. However, this perception also leads employees to over-utilize their benefits as they try to avoid leaving anything unused.

If you offer an HRA that rolls over from year-to-year, employees might be able to avoid the rush to use remaining funds at the end of the year. This strategy promotes longer range thinking. It can also be beneficial at the start of a new plan year when a deductible reset can be overwhelming.

Misconception 2: Employees can be driven to spend.

HRA plan design is a delicate balance. On the one hand, the HRA is intended to support employees’ out-of-pocket expenses. This might be incentive to provide a simple HRA that pays first-dollar coverage. On the other hand, you don’t want to encourage employees to spend more than they need.

So what do you do? Typically, a little shared responsibility with employees will do the trick. Employees need a clear understanding of what their benefits can be used for.

How can you encourage shared responsibility?

There are three effective options to consider for shared responsibility with an HRA Account. Generally, you only need to choose one option. When you start layering on different conditions to your HRA Account, you can have adverse reactions from employees and lower satisfaction.

Option 1: Add a deductible to the HRA.

Adding a basic deductible to the HRA is a good way to curb overuse. Employees pay initial expenses up to the deductible threshold and then the HRA starts paying expenses. Since employees have a little skin in the game, they are less likely to abuse the account and to have a clear understanding of when benefits will be available.

If you choose this option, be careful not to over complicate matters. Make it clear what expenses count towards the deductible. (It is common to include all medical and prescription drug costs). Avoid differentiating between in-network and out-of-network expenses. Embedded deductibles for individual family members can also create complications.

If you are feeling a little progressive, consider a Post-Deductible HRA paired with an HSA.

Option 2: Offer to split the check.

We are in the 21st Century. What is so wrong with splitting the bill?

A “split” or percentage of expense approach to an HRA allows employers and employees to walk hand-in-hand through every expense. A good best practice is to pick a percentage of expenses that the HRA Account will pay and apply it to all eligible expense types. A 50/50 split shows equality between the employer and employees.

Although, if you are feeling a little more generous, a higher employer percentage might earn you a few points. Chivalry is not entirely dead.

Option 3: Treat it like an allowance (or a stipend).

The stipend or flat dollar approach to an HRA can be motivating for employees. Let’s say the plan pays $50 for each visit. Employees now have the decision on how much they want to kick-in. They may choose urgent care services at $75, a doctor’s office at $150 or emergency care at $250.

As the employer, there is a fixed cost for each, but an employee may be motivated to select a lower cost alternative, preventing misuse of funds.

Making a choice

In the end, HRAs can be a maze of decisions. But you can help employees understand the more challenging components of an HRA Account and encourage shared responsibility. There are multiple options to achieve this. How will you choose to route your employees to a path of greater value?